Critical Shifts:

-

The "Affordability Tug-of-War": While average tax refunds are 11% higher than last year (providing a boost to down payments), a 21.2% spike in gasoline prices is simultaneously squeezing monthly budgets. Dealers must pivot their messaging to focus on fuel-efficient units and affordable monthly payments to keep buyers engaged.

-

Shifting Credit Habits: Consumers are becoming more strategic with debt; they are using their larger tax refunds to pay down credit card balances (which grew only 0.1%) while remaining willing to take on non-revolving debt like auto loans. This indicates that while buyers are cautious, they still prioritize vehicle ownership over general consumer spending.

-

Inventory Discipline is Critical: Despite a 17.8% month-over-month increase in new-vehicle sales, they remain down nearly 12% year-over-year. With personal savings rates dipping to 4% and GDP growth slowing, dealers should prioritize tight inventory turn and avoid overpaying at auction to mitigate the risk of a sudden "cooling" after the spring peak.

________________________________________________________

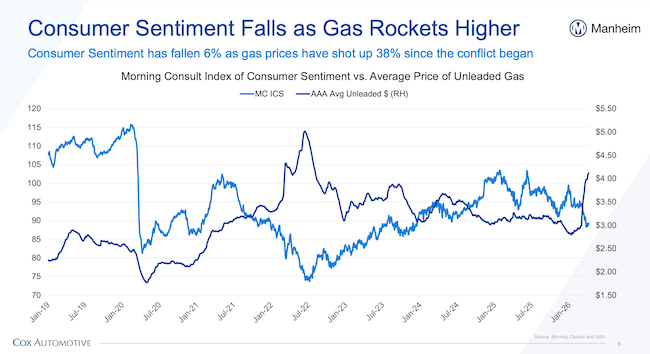

The latest market data reveals a "split personality" for the automotive sector as we move deeper into Q2. For independent and franchise dealers, the current used car market trends are being shaped by a robust tax refund season and a steady wholesale vehicle value recovery, even as consumer purchasing power faces new pressure from a sudden energy price shock and rising headline inflation. While the seasonal "Spring Bounce" is providing a necessary tailwind for the lot, macroeconomic headwinds—specifically a 21.2% jump in gasoline prices—are beginning to test the limits of buyer affordability.

The Bottom Line for Your Lot

March was a month of contradictions. On one hand, your customers are walking in with more cash; the average tax refund is running 11% higher than last year, providing a significant boost to down payments. On the other hand, the Middle East conflict has triggered a massive spike in gasoline prices, pushing the monthly CPI up by 0.9%.

The takeaway: The window to capitalize on "tax season money" is open, but the rising cost of living is making shoppers more sensitive to monthly payments than they were in February.

Wholesale Values & Inventory Strategy

Wholesale values continued to reflect the "Spring Bounce" throughout March. While new-vehicle sales saw a 17.8% month-over-month increase, they are actually down 11.6% compared to March 2025.

-

Pricing Discipline: Manufacturers are keeping new-car transaction prices high (averaging $49,275).

-

The Used Opportunity: As new-car affordability remains strained, the demand for high-quality used units remains your strongest play. However, with real disposable income growth slowing to its lowest level in a year, dealers should be cautious about overpaying for inventory at auction.

The Credit & Spending Shift

The Federal Reserve’s latest report shows a telling shift in how your customers are managing their money:

-

Revolving Credit Slowdown: Growth in credit card debt slowed to just 0.1% in February. This suggests consumers are using those 11% higher tax refunds to pay down balances rather than taking on new debt.

-

Non-Revolving Growth: This sector grew at its fastest pace since late 2025, which includes auto loans. Consumers are still willing to take on structured debt for a vehicle, even if they are pulling back on "swiping the card" for daily expenses.

-

Savings Alert: The personal saving rate has dipped to 4%. Buyers have less of a cushion, making the "gap" between their trade-in value and the next vehicle's price more critical than ever.

Macro Outlook: GDP and the "Affordability Test"

The final look at Q4 2025 GDP confirmed a sharp deceleration to 0.5% growth. While the economy is still expanding, the momentum is cooling. For the used car manager, the next several weeks are a litmus test.

Watch out for:

-

Gas Prices: If gasoline stays at these elevated levels, expect a shift in demand toward smaller, fuel-efficient ICE vehicles and hybrids.

-

Interest Rates: The "financing cost environment" shows no signs of easing. High-APR environment means your F&I office needs to be sharper than ever to hold deals together.

-

Inventory Turn: With the personal saving rate drifting lower, the "Spring Bounce" might end abruptly. Keep your inventory turn tight as we head into May.

The seasonal tailwind is currently fighting a macroeconomic headwind. Dealers who move metal now while refunds are still hitting bank accounts will be in a better position than those waiting for a "summer heatwave" that may be cooled by inflation.