Critical Shifts:

-

Sales Velocity Rebound: The retail sales pace surged in February, with the daily sales rate jumping 13% compared to January (averaging 50,400 units per day).

-

Inventory Tightening: Total nationwide supply dipped 2.6% month-over-month to 2.13 million units, signaling that dealers are moving metal faster than they are replenishing it.

-

The 42-Day Rule: Days’ supply has dropped to 42 days, down seven days from January. This is 11 days lower than the 2022 benchmark, indicating a highly constrained market.

-

Pricing "Soft Spot": The average listing price fell by 1.1% to $25,287. This dip was largely driven by softening prices in the SUV segment, which represented nearly half of all sales.

-

The Affordability Crisis: Units priced under $15,000 are in critical shortage with only a 31-day supply (9 days below the industry average), making them the hardest inventory to source.

-

Macro Drivers: Strong performance was fueled by a "perfect storm" of record-high credit availability (highest since 2022), increased tax refund amounts, and a post-weather rebound.

-

Market Dominance: Five brands—Ford, Chevrolet, Toyota, Honda, and Nissan—continue to own the market, accounting for nearly 50% of all used vehicles sold.

-

CPO Growth: Certified Pre-Owned sales reached 207,263 units, a 2.2% month-over-month increase, as consumers seek value and reliability in a high-interest environment.

________________

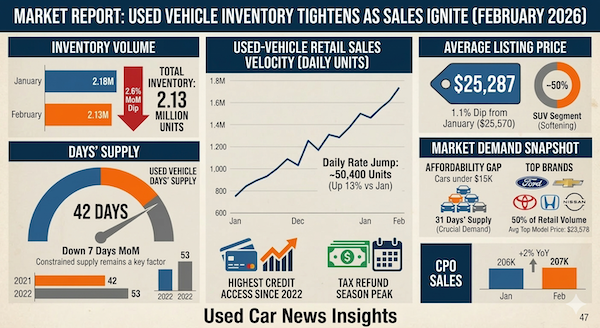

February 2026 proved to be a high-velocity month for the independent and franchised car dealers. According to Cox Automotive’s analysis of vAuto Live Market View data, used-vehicle inventory levels are dipping and retail sales volume are climbing, as auto dealers navigate a market defined by softening listing prices, increased credit availability, and a shrinking days’ supply. This analysis indicates a significant rebound from the early-year slump, fueled by a surge in tax refund season activity..

Inventory Check: Supply Dips as Demand Surges

The total nationwide supply of used vehicles stood at 2.13 million units in February. While this is a 1.6% increase over the same period in 2025, it represents a 2.6% drop from January’s 2.18 million units.

For dealers, this tightening supply is a double-edged sword. While it indicates healthy movement on the lot, the days’ supply has plummeted to 42 days—down seven days from January and a significant 11 days lower than February 2022.

Sales Velocity: A 13% Daily Jump

The retail pace was the standout metric for the month. Estimated sales volume hit 1.41 million vehicles, up from 1.38 million in January. More impressively, the daily sales rate jumped 13% month-over-month, averaging 50,400 units sold per day.

What’s driving the floor traffic?

-

Tax Refunds: Higher-than-average refund amounts are hitting consumer bank accounts.

-

Credit Access: Credit availability has reached its highest peak since 2022, easing the path for subprime and near-prime buyers.

-

Price Softening: Average listing prices dropped 1.1% from January, settling at $25,287.

The "Affordability Gap" Continues

Independent dealers specializing in budget-friendly units face a persistent challenge: sourcing. Vehicles priced under $15,000 remain incredibly scarce, sitting at a razor-thin 31-day supply.

Meanwhile, the "Big Five" (Ford, Chevrolet, Toyota, Honda, and Nissan) continue to dominate the lanes, accounting for nearly 50% of all retail volume. The top-selling models averaged a listing price of $23,578, nearly 7% below the national average, proving that the $20k–$24k sweet spot is currently the market's "power zone."

CPO Momentum

The Certified Pre-Owned (CPO) segment also saw a boost, with sales rising to 207,263 units. This 2% year-over-year increase aligns with a broader trend of consumers seeking "new-car peace of mind" at used-car price points as new-vehicle inventory fluctuates.

Dealer Takeaway

With inventory shrinking and sales rates accelerating, the window to replenish lots at "softened" prices may be closing. Dealers should focus on high-turnover brands and aggressive financing options to capitalize on the current peak in consumer credit and tax-season liquidity.