Key Insights:

-

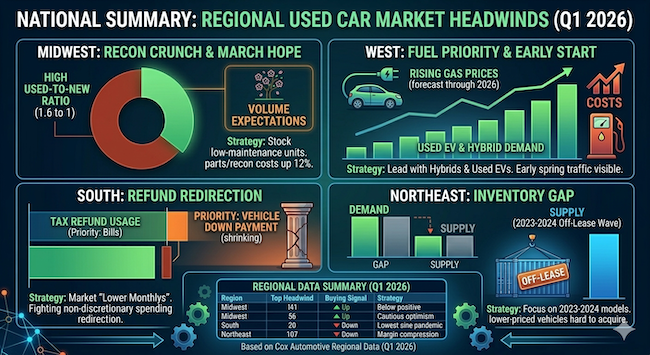

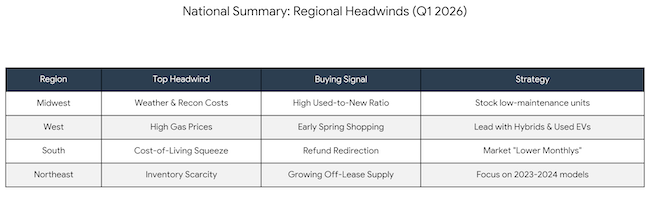

Tax Refund Tailwind: The average 2026 tax refund is $3,742 (up 10.6%), injecting significant purchasing power into the used car market this March.

-

Wholesale Value Surge: The Manheim Used Vehicle Value Index (MUVVI) hit 212.3 in February, its highest level since 2023, signaling that acquisition costs are rising as the spring season heats up.

-

The Used EV "Paradox": While new EV sales struggle with the loss of incentives, used EV sales spiked 21% in January, with Audi (up 63.4%) and Tesla leading the volume.

-

Inventory & Margin Pressure: Used vehicle inventory remains tight at a 45 index score, forcing independent dealers to navigate higher auction prices while retail traffic remains near pandemic-era lows (index of 28).

-

Economic Headwinds: Sudden geopolitical tensions pushed gas prices up 13% in one week, arriving just as a cooling labor market (92k jobs lost in February) adds a layer of caution to big-ticket purchases.

________________

The Q1 2026 Cox Automotive Dealer Sentiment Index (CADSI) reveals a "spring bounce" in optimism for the used car market, even as independent dealers navigate a complex landscape of rising wholesale vehicle values, shifting consumer credit growth, and sudden geopolitical tensions impacting gas prices.

While the Manheim Used Vehicle Value Index (MUVVI) surged to its highest level since 2023, the industry is closely watching how record-high tax refunds will compete with a cooling labor market and inflationary headwinds.

The "Spring Bounce" Meets Wholesale Reality

The typical seasonal lift is underway, with the overall future outlook index jumping to 56 from a dismal 42 in Q4. However, for the used car specialist, the road is paved with "cautious optimism." While used-vehicle inventory remains tight at a 45 index, demand at auction is heating up.

According to the latest Manheim Used Vehicle Value Index, wholesale values rose to 212.3 in February. Prices jumped 3% month-over-month, a move significantly stronger than typical seasonal patterns. For dealers, this means the cost of acquiring units is rising fast: MMR prices for three-year-old vehicles surged 3.1% in February alone.

“Since the start of 2026, we’ve seen mostly solid demand at Manheim with higher sales conversion rates indicating an appetite from dealers to buy,” said Jeremy Robb, Chief Economist at Cox Automotive. “As we progressed through February, we saw prices move higher than usual.”

The Used EV Surprise: A Bright Spot Amidst New EV Struggles

While new EV sentiment plummeted to a record low of 33 following the expiration of federal incentives, the used EV market is telling a much more aggressive growth story.

-

Sales Volume: Used EV sales hit 31,503 units in January—a 21.2% increase year-over-year.

-

Market Share: Used EVs now represent 2.1% of the total used market.

-

Top Performers: Tesla continues to dominate the pre-owned electric space with over 12,400 units, but Audi saw the most explosive growth, surging 63.4% month-over-month to displace Nissan in the top five.

This suggests that while high MSRPs and lost tax credits are hurting new EV showrooms, value-conscious shoppers are increasingly turning to the secondary market for electric mobility.

Tax Refunds vs. Gas Prices: The March Tug-of-War

The used car industry’s biggest "tailwind" is currently the IRS. The average tax refund is currently $3,700—up 10.6% from last year. With $137 billion already returned to consumers, the purchasing power for a used vehicle down payment is at its highest level in years.

However, new "wildcards" have emerged:

-

Geopolitical Friction: Tensions in the Middle East caused gas prices to jump 13% in a single week to $3.46.

-

Labor Market Cooling: The economy shed 92,000 jobs in February, creating a "fragile backdrop" for discretionary spending.

-

Interest Rate Reversal: The 10-year Treasury rose more than 10 basis points, signaling that the "relief" dealers were hoping for may be delayed as markets price in a more inflationary environment.

The Independent Dealer Perspective

The Independent Dealer Perspective

While franchised dealers reported a market index of 48, independent dealers remain more cautious as profitability (32) and customer traffic (28) remain under extreme pressure. Rising operational costs and decelerating consumer credit growth (1.9%) mean that while the "intent" to buy is there, the "ability" to finance remains the primary hurdle.

“The key question for March is whether that momentum can hold in the face of rising gas prices and a softer labor market,” noted Robb. For now, used car dealers are banking on the "tax refund bridge" to carry them through a volatile start to the year.