Critical Shifts:

-

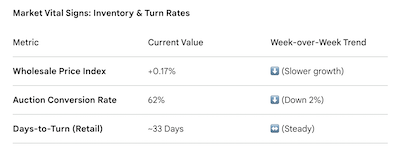

Selective Buying & Softening Conversions: While wholesale prices rose slightly (+0.15% to +0.17%), the auction conversion rate fell to 62%. Dealers are becoming more disciplined, moving away from broad bidding and focusing strictly on high-quality, retail-ready units.

-

The Mid-Size Rebound vs. Luxury Lag: Mid-size cars are proving to be a safe bet, rebounding with a +0.30% gain and showing growth in ten of the last twelve weeks. Conversely, the luxury segment continues to soften, declining in nine of the last twelve weeks—dealers should exercise caution when stocking high-end sedans.

-

Inventory Velocity Check: The average Days-to-Turn is currently 33 days. With small pickups ending a 10-week growth streak and compact crossover gains moderating, the market is shifting toward a "unit-specific" value model where mileage and trim configuration matter more than general segment trends.

_____________________________________________________

Black Book's Market Insights for the week ending April 18th suggests a shift in the lanes, with wholesale price trends showing a "stable but selective" environment. For independent and franchised dealers, the used car market analysis reveals that while wholesale vehicle values saw modest gains—with cars up +0.15% and trucks up +0.17%—the auction conversion rate dipped to 62%. This indicates that while used car inventory remains in demand, buyers are exhibiting increased discipline, focusing heavily on retail-ready units and late-model SUVs rather than bidding up the broader market.

Car Segment: Mid-Size Rebounds, Luxury Lags

Inventory managers should take note of the divergence in the car market. While younger cars (0-2 years) saw the most aggressive price movement, the real story is in the Mid-Size and Luxury categories.

-

Mid-Size Strength: After a brief dip, Mid-Size cars bounced back with a +0.30% gain. This segment has been a winner in ten of the last twelve weeks, signaling sustained retail demand for affordable, fuel-efficient commuters.

-

Luxury Softness: In contrast, the Luxury Car segment has declined in nine of the past twelve weeks. If you are stocking high-end sedans, be wary of overpaying at auction as this segment continues to average a -0.06% weekly decrease.

-

Older Units: The 8-to-16-year-old "budget" units remain a safe bet for many lots, posting a healthy +0.27% increase as floor-planned buyers chase lower price points.

Truck & SUV Segment: Compacts Cool Off, Small Pickups Slip

The truck market remains the primary driver of wholesale activity, though the frantic pace of the previous week (+0.33%) has slowed to a more sustainable +0.17%.

-

Crossover Moderation: Compact Crossovers rose +0.18%, a significant cooling from the +0.68% jump seen the week prior. However, with gains in 11 of the last 12 weeks, these remain the "bread and butter" for most used car operations.

-

Small Pickup Warning: After ten consecutive weeks of growth, the Small Pickup segment finally hit a ceiling, dropping -0.08%. Dealers should exercise caution when bidding on these units to avoid being "all-in" on a cooling asset.

-

Late-Model Stability: 2023–2024 units are trading mostly in the clean-to-average range. Even with low mileage, some mid-trim crossovers are showing signs of softening, reinforcing the need for careful physical inspections.

The "Bottom Line" for Dealerships

The current wholesale environment is no longer a "rising tide lifts all boats" scenario. With the Days-to-Turn sitting at 33 days, the pressure is on to buy right at the auction. Buyers are showing a limited willingness to stretch on pricing, and outcomes are now heavily tied to unit-level factors like specific trim configurations and mileage rather than broad segment momentum.