With negative equity at an all-time high (58%) and subprime access opening up, the "easy" deals are gone. Use these talking points and strategies to get your desk bought.

1: The "Behavioral Finance" Approach (Recalibration)

-

The Trend: Current lending models capitalize on "instant gratification" and low-friction entry points, much like digital subscription models, to build user dependency.

-

F&I Tactic: When a buyer hits a wall with "rate shock," reframe the conversation as a macro-economic "transition phase." Deflect the focus from the high-interest "pain point" and anchor the value back to the vehicle’s utility as an essential tool for their daily productivity.

-

The Pivot: "We’re in a unique market recalibration right now. Our goal is to secure the asset you need today. Let's focus on a 12-month stability plan, then we can look at a refinance strategy once the market cycle settles."

2. Managing the "Upside-Down" Trade (The 58% Rule)

-

The Trend: Nearly 60% of your customers are underwater.

-

F&I Tactic: Don't wait for the box to discuss negative equity.

-

Early Disclosure: Have Sales confirm the payoff before the test drive.

-

The "Gap" Close: With record negative equity, GAP insurance is no longer an "upsell"—it’s a necessity for consumer protection. Frame it as: "Because you’re carrying $X in negative equity, your insurance only covers the car's value, not your loan. We need to bridge that gap today."

-

3. Leveraging the Subprime Appetite

-

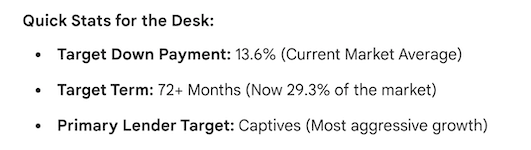

The Trend: Captives and Finance Companies are hungry for subprime (17.5% share).

-

F&I Tactic: * Submit to Captives First: Captives are leading the loosening (up 3.9%). They are currently more aggressive than banks.

-

The 72+ Month Bridge: Use the record-high 72+ month terms as a tool, not a crutch. If a customer is wary of the long term, remind them it provides the lowest required monthly obligation, but they can always pay more toward the principal when they have "extra" to shorten the effective term.

-

4. Inventory Positioning: The $20k Sweet Spot

-

The Trend: "Payment Buyers" are back.

-

F&I Tactic: If a deal is struggling on a $30k unit due to the 11.2% average rate, have a "Plan B" unit under $20k ready. The math on a $20k car at 11% is much easier for a subprime lender to swallow than a $30k car with $6k in rolled-over negative equity.

_________________________________________________