Critical Shifts:

-

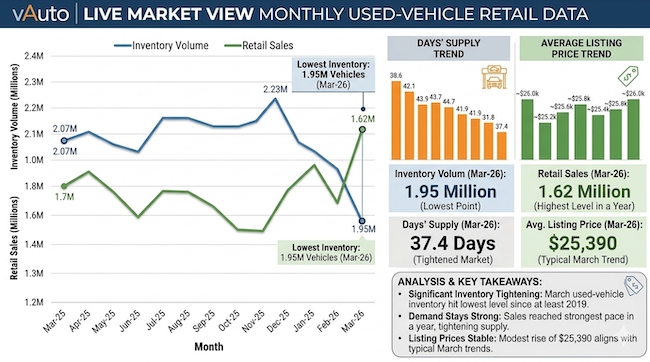

Historic Inventory Drought: Used-vehicle supply has hit its lowest level since 2019, with total volume dropping to 1.95 million units and a tight 37-day supply (plunging even lower to 27 days for vehicles under $15k).

-

EVs Outpacing the Market: Buoyed by gas prices exceeding $4 per gallon, used EV values rose 6.2% year-over-year, significantly outperforming the 1.7% appreciation seen in the non-EV segment.

-

Wholesale Normalization: While Q1 started "hot," the seasonal spring bounce is tapering off; wholesale prices saw a 1.1% dip in early April, signaling a shift toward more typical depreciation patterns for the second quarter.

___________________________________________________

Independent auto dealers are navigating a paradox of "high demand and low supply" as the spring selling season reaches its peak. According to the latest data from Cox Automotive’s vAuto Live Market View and the Manheim Used Vehicle Value Index (MUVVI), the industry is grappling with the lowest used-vehicle inventory levels since at least 2019, while retail demand continues to tighten the market.

Inventory Hits Record Lows

Nationwide, total used-vehicle supply plummeted to 1.95 million units in March—a 5.9% year-over-year decline. This marks the third consecutive month of shrinking inventory, leaving lots at their emptiest since the current data set began seven years ago.

The crunch is most visible in the "days’ supply" metric, which dropped to 37 days in March. This is a significant 7-day drop from February and the lowest reading since 2021. For independent dealers focusing on the budget-conscious segment, the news is even more stark: vehicles priced under $15,000 are operating on a razor-thin 27-day supply.

Retail Performance: Tax Refunds Fuel the Fire

Despite the scarcity of units, sales volume in March reached its highest level in a year, estimated at 1.62 million vehicles. "March is typically the strongest month of the year for used-vehicle sales, and 2026 was no exception," Scott Vanner, Cox Automotive Manager of Economic and Industry Insights, noted.

Healthy tax refunds and a "strong value proposition" compared to high new-vehicle prices kept consumers in the market. While sales were down slightly (2.9%) compared to last year's tariff-driven surge, they outperformed 2023 and 2024 levels.

Wholesale Trends: The "Spring Bounce" Cools

In the wholesale lanes, the red-hot momentum of the first quarter is beginning to normalize. The Manheim Used Vehicle Value Index (MUVVI) decreased to 213.0 in the first half of April, a 1.1% dip from March. However, values remain 2.3% higher than they were this time last year.

Jeremy Robb, Chief Economist at Cox Automotive, suggests the seasonal peak may be behind us. "We started 2026 off hot... wholesale prices are still rising but at much more normal levels relative to long-term averages," Robb said. He noted that while seasonal appreciation is tapering off, sales conversion rates remain high at 65%, indicating that demand at auction is still robust.

Key Market Drivers for Dealers to Watch

-

The EV Edge: Electric vehicles are bucking the trend. The EV Index rose 6.2% year-over-year, outperforming non-EVs (up 1.7%). With gas prices hovering above $4 per gallon, used EVs are seeing higher appreciation as dealers test consumer demand elasticity.

-

Listing Prices: Average retail listing prices remained stable at $25,390, a modest 0.7% increase from February.

-

The "Big Five" Dominance: Ford, Chevrolet, Toyota, Honda, and Nissan continue to dominate the used market, accounting for 51% of all sales. The top sellers averaged a price of $23,861, roughly 6% below the industry average.

-

CPO Slowdown: Certified Pre-Owned (CPO) sales took a hit, falling 11.2% year-over-year. This suggests that price-sensitive buyers may be moving toward non-certified units to stay within their budgets.

The Bottom Line for Independent Dealers

The market is currently a "seller's market" in terms of demand, but a "buyer's nightmare" for sourcing. With wholesale supply holding steady at 25 days and retail supply at record lows, the challenge for the second quarter will be inventory acquisition. As seasonal appreciation winds down, dealers should watch for "elevated depreciation rates" in late April to potentially find better entry points for fresh stock.