Critical Shifts:

-

Increased Consumer Purchasing Power: For the first time in years, "sticker shock" at the insurance desk is receding. With a nationwide 5% moderation in actual policy costs, buyers—particularly in the subprime or budget-conscious segments—have more room in their monthly budgets to absorb vehicle financing costs.

-

Transaction-Based Data vs. Quotes: Unlike standard industry forecasts based on "estimates," this data is pulled from actual bound policies. For dealers, this means the relief isn't just theoretical; it represents real-world savings that your customers are already seeing when they sign for coverage to drive off your lot.

-

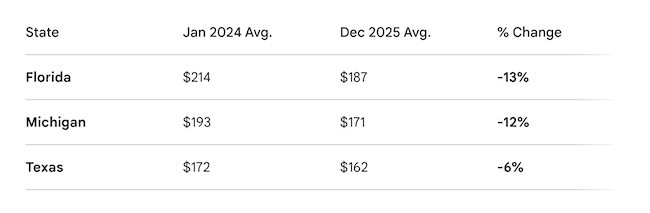

Regional "Hot Spots" for Sales Growth: Dealers in Florida (-13%), Michigan (-12%), and Texas (-6%) are seeing the most aggressive market corrections. If you are operating in these states, the "total cost of ownership" argument is currently a powerful marketing tool to re-engage leads who walked away from deals in 2024 or 2025 due to high carrying costs.

__________________________________________

HUNTINGTON BEACH, Calif. — For independent auto dealers, the "sticker shock" hasn't just been on the windshield—it’s been in the insurance office. However, new data suggests the tide may finally be turning, potentially removing a major hurdle for credit-challenged and cost-conscious car buyers.

Freeway Insurance has released a comprehensive 2026 report revealing that insurance costs in several high-volume states are beginning to moderate after years of aggressive hikes. Unlike typical industry forecasts based on "quotes," this report analyzes actual policy purchase transactions—the real dollars your customers are paying to drive off the lot.

The Numbers: A Downward Trend

The analysis, which tracks data from 2024 through the end of 2025, shows that average costs dropped by nearly 5% across key markets. For dealers in states like Florida and Michigan, the relief is even more pronounced:

Why This Matters for Your Dealership

Lower insurance premiums directly increase a buyer's purchasing power. In an environment where interest rates and vehicle prices remain high, a double-digit drop in monthly insurance costs can be the difference between a "dead deal" and a closed sale.

"Markets that experienced the steepest increases in recent years are now seeing the most noticeable corrections," the report notes. This suggests that the "uninsurable" price peaks of the last few years are finally eroding.

Real Data, Real Sales

Because Freeway’s report is based on actual binding payments rather than estimates, it serves as a "canary in the coal mine" for the industry. For independent dealers, this data is a tool to help reassure hesitant buyers that the total cost of ownership is becoming more manageable.

As the largest personal lines insurance distribution platform in the U.S., Freeway Insurance continues to leverage its carrier partnerships to find affordable coverage options, helping more drivers—and more of your customers—get on the road.